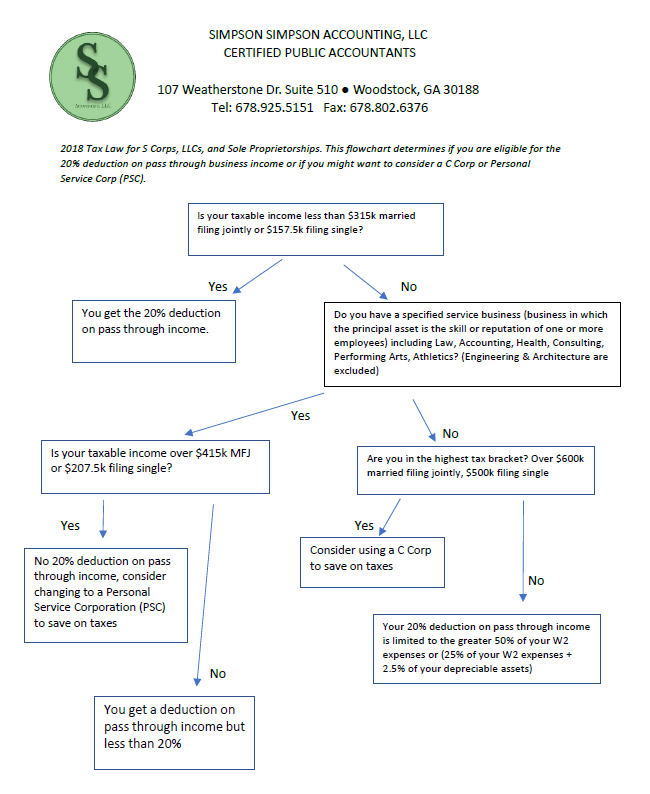

Since the 20% deduction for qualified business income is not so easy to follow, we created a flowchart to try and provide some clarity. The key word here is “try”. Kind of goes against the buzz phrase, “Your tax return will fit on the back of a post card” 🙂

As you can see, it takes a second to figure out how it works. When we first looked at the calculation, it didn’t seem that beneficial. But after taking a closer look and running the numbers on some of our existing business clients, it is generous.

One reason it is generous is that the 20% deduction is reduced based on “taxable income” being over $315k married filing jointly/$157.5k single, not “adjusted gross income”.

So, the taxpayer/s will reduce their adjusted gross income with the new double standard deduction of $24k (Or more if itemized deductions were greater than $24k) before checking if they are under the $315k/$157.k threshold.

On a side not, a lot of people will be enticed to change their business to a C Corp in 2018 but be careful! Have a CPA firm run the numbers first.

It might only make sense for business owners with taxable income in upwards of $600k or business owners that are okay with only a W2 and don’t need to take dividend distributions. The thing to remember about a C Corp is that it is double taxed. The income is taxed inside the C Corp at the new 21% rate but also taxed once taken out of the C Corp as dividends at an approximate rate of 20%.

The C Corp will work great in 2018 and beyond if okay with leaving money inside the C Corp.

Lots of moving pieces here, strongly recommend running the numbers on the full business/personal tax situation to see what works best!